The US labour market is losing momentum – as is the USD

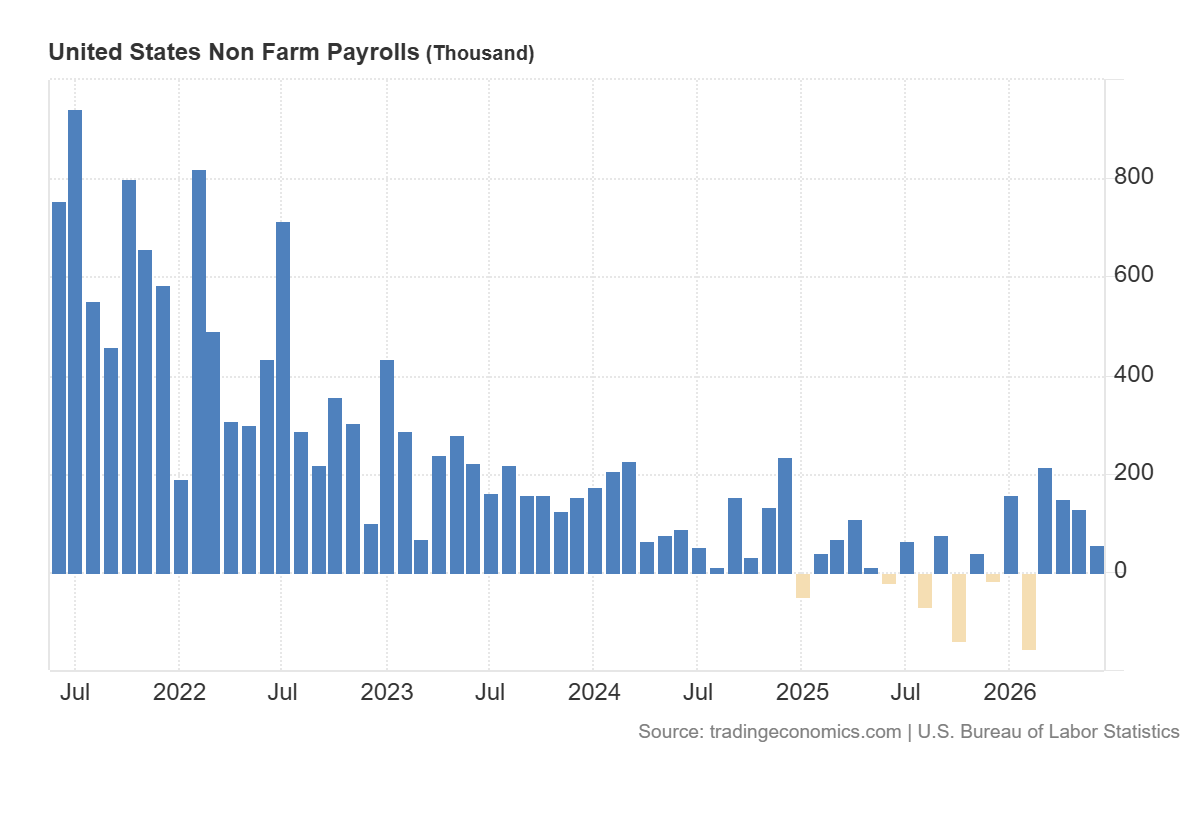

- The U.S. labor market is losing momentum, but not collapsing. Nonfarm payrolls rose by only 57,000, previous months were revised lower, and hiring has clearly slowed, while layoffs remain limited.

- The drop in unemployment is less positive than it looks. The unemployment rate fell to 4.2%, but this was partly due to a decline in labor force participation to 61.5%, meaning some people stopped actively looking for work.

- The report reduced pressure on the Fed to tighten policy further. Slower job growth and easing wage pressure revived hopes for future rate cuts, weakened the dollar, and supported assets such as gold, Bitcoin, and EUR/USD.

June data from the U.S. labor market showed a clear weakening in employment momentum. Nonfarm payrolls increased by only 57,000, significantly below economists’ expectations. In addition, data for the previous two months were revised downward, weakening earlier signals that had suggested greater resilience in the labor market.

At first glance, the decline in the unemployment rate to 4.2% appeared positive. However, this is not an unambiguous sign of improvement. The drop in unemployment was accompanied by a marked decline in labor force participation. The participation rate fell to 61.5%, reaching its lowest level in more than five years. This means that some individuals stopped actively looking for work and were therefore no longer included in unemployment statistics.

Companies are not conducting mass layoffs, but they are hiring more cautiously

The report does not point to a labor market collapse, but it does show increasing caution among employers. Initial jobless claims remained almost unchanged, suggesting that the scale of layoffs remains limited. The issue, therefore, is not a sharp reduction in employment, but a weaker willingness among companies to create new jobs.

The largest decline in employment was recorded in the leisure and hospitality sector. This is particularly important because, at this time of year, the industry typically increases seasonal hiring. Weaker-than-usual employment growth may indicate a more cautious approach by companies toward consumer demand and future operating costs.

At the same time, some sectors continued to support the labor market. Healthcare and social assistance remained the main source of employment growth. Job numbers also increased in manufacturing and construction. Weakness persisted, however, in the information sector, where employment declined for the seventeenth time in the past eighteen months.

Wages are rising, but inflationary pressure is easing

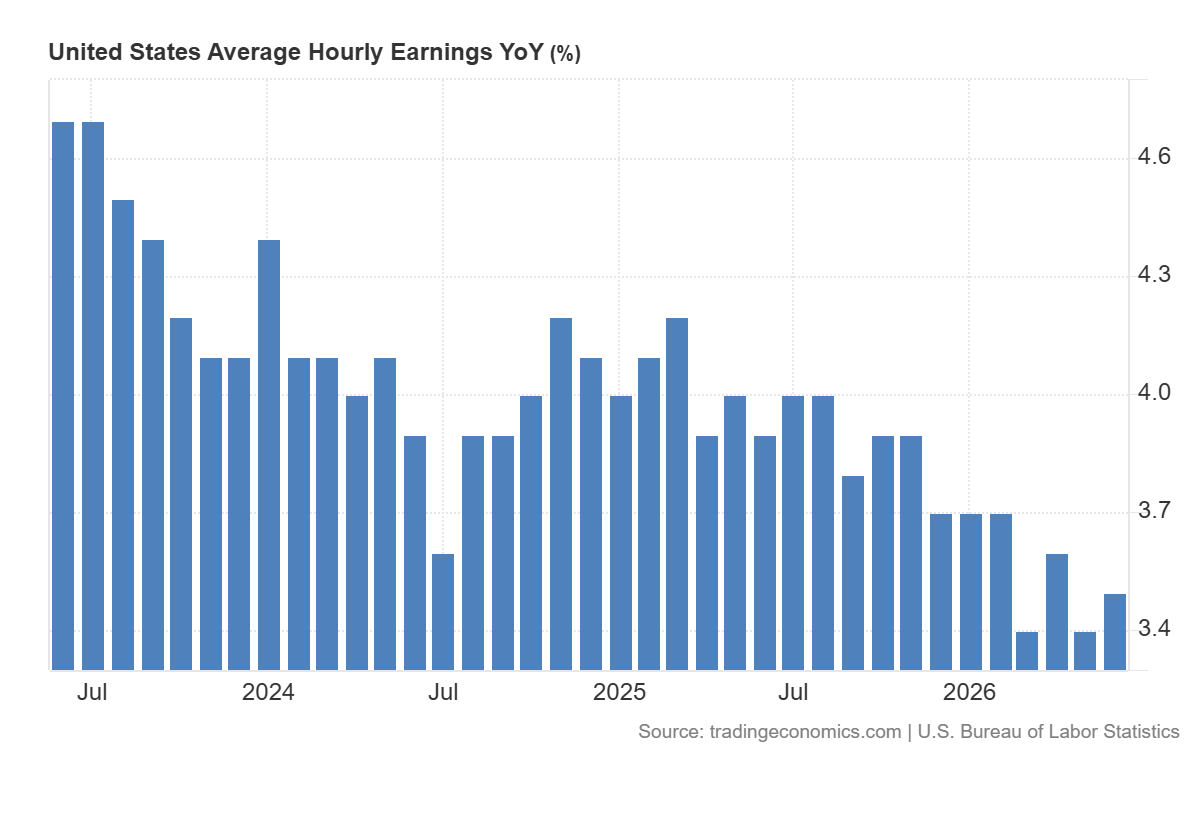

Average hourly earnings rose by 3.5% year over year in June. This increase shows that wages are still growing, but they are no longer generating inflationary pressure as strong as during the period of peak labor market tightness. For the Federal Reserve, this may be an argument that employment conditions remain relatively stable and do not require an abrupt policy response.

From the perspective of households, however, the picture is less favorable. Slower employment growth means fewer opportunities to find a new job, while inflation continues to limit the real purchasing power of wages. Even if nominal wages are rising, many workers may not feel a clear improvement in their financial situation.

Markets took note of the report’s weakness

The release triggered a moderately positive reaction in financial markets. The S&P 500 opened higher, while U.S. Treasury yields declined. Investors scaled back expectations for further interest rate hikes by the Fed, although they still priced in at least one rate increase this year.

The market reaction shows that weaker employment data were interpreted as a factor reducing pressure on the central bank. If the labor market continues to lose momentum, the Fed may have fewer reasons to tighten monetary policy further.

A mixed picture of the U.S. economy

The data were disappointing, but they should not fundamentally change the overall assessment of the economy. The labor market reflects uneven economic growth, in which some sectors are still creating jobs while others are clearly slowing. From the Fed’s perspective, the situation does not look alarming, as the labor market is not generating additional inflationary pressure. For American households, however, it means more difficult conditions, especially when limited employment opportunities coincide with persistently high living costs.

Kevin Warsh’s first press conference as FOMC Chair was perceived as hawkish and fueled concerns about an interest rate hike in the United States. As a result, the dollar strengthened significantly in recent weeks. Following today’s NFP report, hopes for an interest rate cut have resurfaced. Of course, with core PCE inflation currently at 3.4% year over year, this remains unlikely. Nevertheless, today’s reading creates a balance between arguments for monetary easing and monetary tightening, given the Fed’s dual mandate of maximum employment and price stability. It was precisely these hopes that led to a weakening of the dollar. EUR/USD is currently trading at 1.1446, up 0.59%. Instruments quoted in USD, which have recently failed to generate returns for investors, also deserve attention. Gold is up 2.37% today, while Bitcoin has gained 2.64%.

A labor market without collapse, but also without strength

The June report shows that the U.S. labor market is in a phase of clear slowdown. There are no signs of mass layoffs or a sharp deterioration in conditions, but it is becoming increasingly difficult to describe the market as strong. Companies are acting cautiously, new jobs are being created more slowly, and the decline in unemployment is partly the result of lower labor force participation.

The key takeaway from the report is therefore that the labor market is not collapsing, but it is losing resilience. For the Fed, this means less pressure from wages and employment, while for workers it means more challenging job-search conditions and limited improvement in real incomes.

Opinions are the authors'; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. The provided publication is for informational and educational purposes only.

If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please refer to the MarketPulse Terms of Use.

Visit https://www.marketpulse.com/ to find out more about the beat of the global markets.

© 2026 OANDA Business Information & Services Inc.